"The answer for developed markets, however, remains elusive. The offerings for developed markets will take a different format," Ms. Shen said. "Instead of a point offering for mobile payment, the service needs to be built on top of the existing payment behavior and infrastructure so that users can choose any channel - retail, phone, online or mobile - that suits their context at the moment of payment."

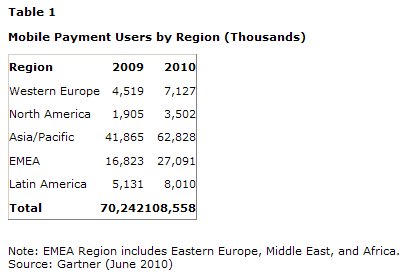

Asia/Pacific is the leading region with mobile payment users. In Asia/Pacific, mobile payment users will surpass 62.8 million in 2010 (see Table 1), and represent 2.6 percent of all mobile users. In Europe, the Middle East and Africa (EMEA), mobile payment users will total 27.1 million and represent 2.1 percent of all mobile users in the region. In North America, mobile payment users will number 3.5 million and represent 1.1 percent of all mobile users in the region.

Ms. Shen said that the strong demand for mobile payment in developing markets is being driven by the unbanked and underbanked populations that do not have ready access to the banking infrastructure or PC, positioning mobile as the natural choice of access platform. At the same time, regulators in early-adopter markets are tightening up policies to provide better user protection and fight against unlawful financial activities relating to money transfer.

Short Message Service (SMS) remains the dominant mobile payment technology. Its ubiquity and ease of use makes it the technology of choice, not only for consumers in developing markets, but also for those in developed markets. Wireless Application Protocol/Web can support either downloadable clients or mobile browsers. It is more frequently used by consumers in developed markets due to the higher penetration of data-capable phones and active data plans.

Many financial institutions have failed to see the business case of Near Field Communication (NFC) payment, in particular, which offers similar functionality to contactless cards but with the added complexity of dealing with mobile carriers and other ecosystem partners.

Ms. Shen urged service providers in developing markets to investigate service interoperability to speed market uptake and foster healthy competition. She said that solution providers should ensure platform flexibility so that platforms can work with both the bank's and mobile carrier's systems, and so that it can be readily customized for local deployments.

Other interested parties will include financial institutions, which can use mobile payment to reach the unbanked and underbanked populations that cannot be easily reached with the traditional infrastructure. They will need to collaborate with mobile carriers in developing markets to take advantage of their brand recognition and service coverage. In developed markets, they should work with large retailers and online merchants to build on existing purchase and payment behavior.